Introduction

On January 17, the National Bureau of Statistics (NBS) released macroeconomic and real estate sector data for December and the whole year. Meanwhile, the Information Office of the State Council held a press conference on the same day, and Kang Yi, the director of the National Bureau of Statistics, answered a reporter's question on the operation of the national economy for the whole year of 2023:

From the current situation, there are some positive changes in the real estate market, mainly in two aspects: first, the decline in real estate investment, sales and other indicators narrowed. 2023, real estate development investment fell 9.6% compared with the previous year, the decline rate narrowed by 0.4 percentage points compared with the previous year; real estate development enterprises in place of the funds fell 13.6%, the decline rate narrowed by 12.3 percentage points compared with the previous year; the sales area of commercial properties and the Sales amount of commercial properties fell 8.5% and 6.5%, down 15.8 and 20.2 percentage points narrower than the previous year. Second, the real estate completion area increased faster. The work of "guaranteeing the delivery of buildings" is steadily advancing, and the effect continues to show. 2023, the completed housing area of real estate development enterprises increased by 17% over the previous year.

Specifically:

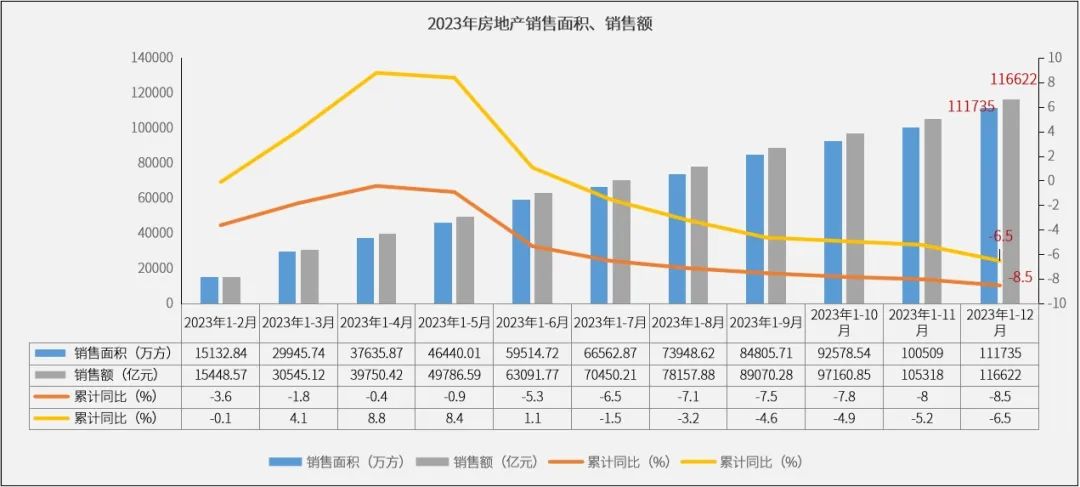

Data from the National Bureau of Statistics showed that the annual sales area of commercial housing in 2023 was 1.117 billion square meters, down 8.5% compared with 2022, a decline of 15.8 percentage points narrower; the sales value of commercial housing was 11.66 trillion yuan, down 6.5% compared with 2022, a significant narrowing of the decline rate of 20.2 percentage points.

At the beginning of 2023, the market rebounded rapidly with the addition of a mini-sunrise, but the market has been gradually downward since the second half of the year. Even with the introduction of a series of favorable policies, as well as the further reduction of the cost and threshold for purchasing homes to enter the market, the industry as a whole still maintained a bottomward oscillation pattern. The sales area of commercial housing returned to the level of 2014, while the sales value was slightly higher than that of 2016. Compared with the industry's peak in 2021, the area decreased by 38% and the amount decreased by 36%.

▲ Source: National Bureau of Statistics

▲ Source: Wind

Affected by the epidemic, weak sales and the liquidity risk of real estate enterprises and many other factors, the past two years, the area of new construction showed a cliff-like decline. 2023, the national real estate new construction area of 954 million square meters, down 20.4% year-on-year, residential new construction area of 693 million square meters, down 20.9%, the size of the new construction for a new low since 2013.

Among them, the new construction area in a single month in November increased by 3% year-on-year, the first time since March 2021 to achieve growth, mainly and new construction rebound is mainly related to the Q4 rush to start construction around the world, but December year-on-year and fell back.

▲ Source: National Bureau of Statistics

▲ Source: Wind

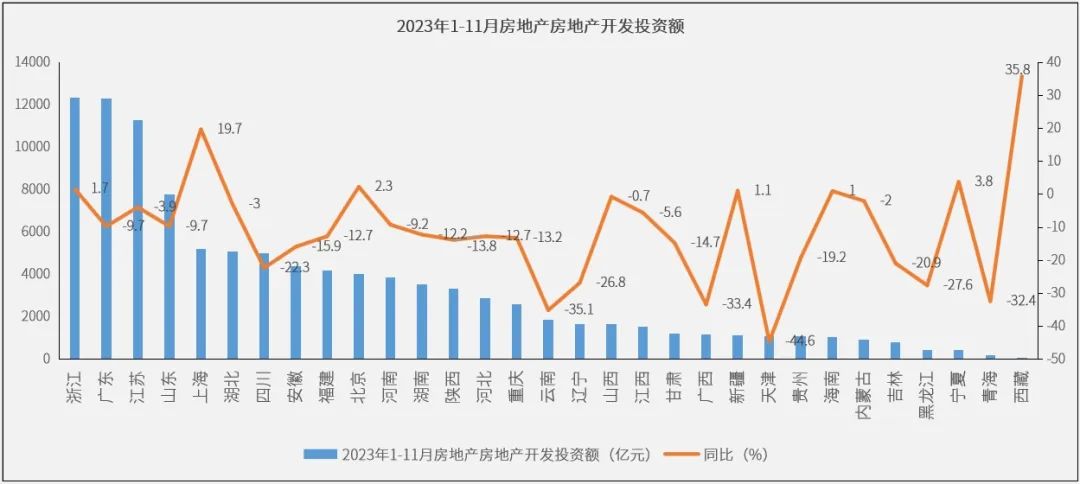

Real estate development investment continued to come under pressure in 2023.In 2023, the national real estate development investment amounted to RMB 11.1 trillion, down 9.6% year-on-year. In absolute terms, the scale of development investment declined for two consecutive years, returning to the 2018 level. Mainly due to the pressure on the capital situation of real estate enterprises in recent years, real estate enterprises are cautious in taking land, and real estate enterprises are weak in their willingness to invest, and their operational focus is on de-stocking and preserving the building.

Among them, real estate development investment amounted to 686.8 billion yuan in December, down 15.4% sequentially, with the absolute amount being a new monthly low in the past ten years, and down 27.3% compared with the average value of the first November of 2023. Year-on-year, on the other hand, it fell 12.5%, a decline that widened by nearly 2 percentage points from November.

▲ Source: National Bureau of Statistics

▲ Source: Wind

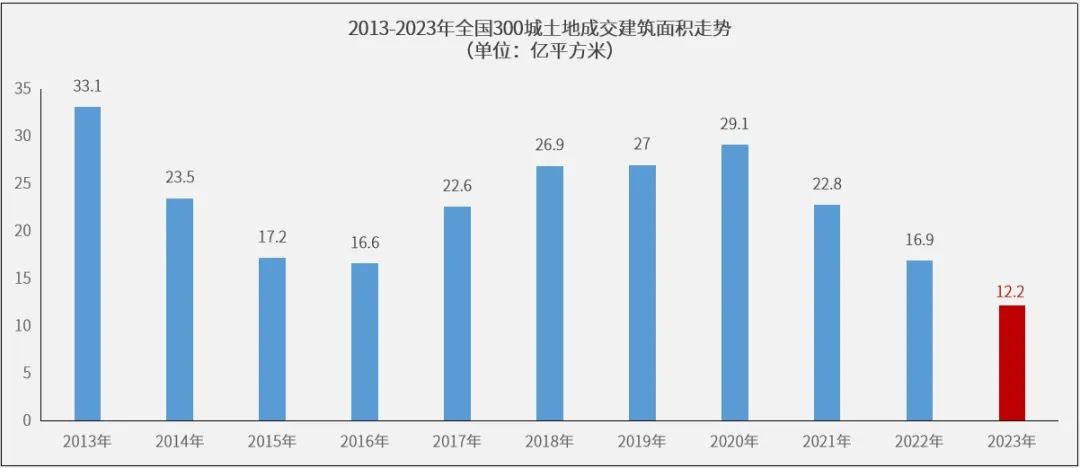

According to the report, as of December 20, 2023, the land market in 300 cities across the country sold 1.22 billion square meters of floor space, down 21% from the same period in 2022, and narrowed by 5 percentage points from the previous year. Even if the December "tail-raising factor" phenomenon as expected, but in the land market continues to be cold, the December transaction scale with the same period last year is not much different. Under this influence, the year-on-year decline in the land market turnover scale in 2023 was maintained at about 20%, and the total turnover scale was a new low in the past ten years.

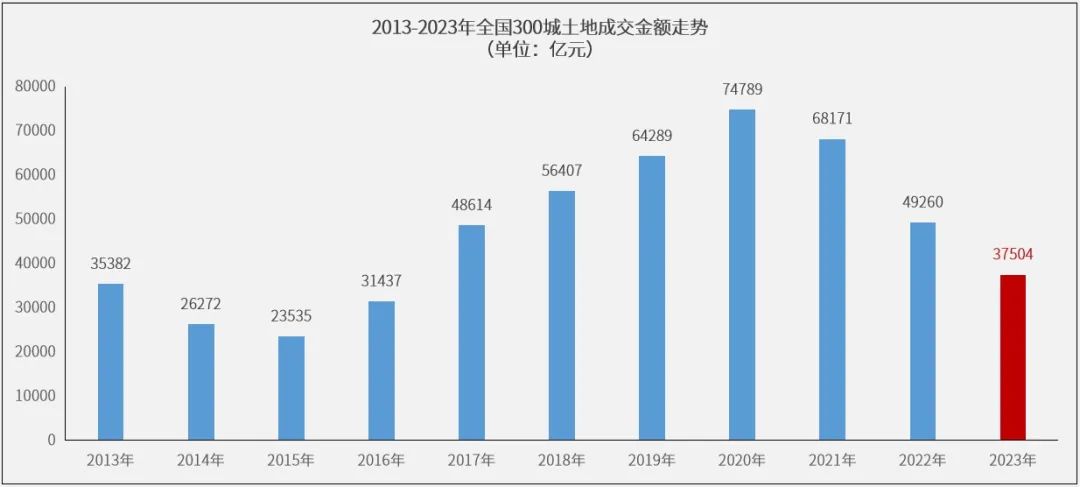

Consistent with the change in land transaction scale, the transaction amount also contracted significantly compared to the same period last year: as of December 20, 2023, the total land transaction amount of 3,750.4 billion yuan nationwide, a year-on-year decline of 18%. The year-on-year decline continued at a high level, mainly due to the land market has continued to be cold since the end of last year, resulting in local governments to be more cautious on the land supply side, the demand side of the enterprise's willingness to take the land has also significantly contracted, the land transactions are mostly at the bottom of the price of the transaction, the transaction amount compared to the same period last year there is still a large gap.

▲ Source:CRIC

▲ Source:CRIC

Due to the cold market environment, the land sales area of each city was lower than that of the same period last year:

As a result of the cold market environment, the land transaction area of cities at all levels was lower than that of the same period of last year. Among them, the total transaction area of first-tier cities was 26.1 million square meters, down 32% from the same period last year. From a city-by-city perspective, in addition to Beijing's transaction size increased by 18% year on year, the transaction size of the remaining three first-tier cities was not equal to that of the same period last year, of which Shenzhen's transaction size decreased by as much as 75% year on year, and Shanghai and Guangzhou's transaction size decreased by nearly 30% and 40% year on year, respectively.

Second- and third-tier cities, the transaction size year-on-year were downward trend, compared with the same period last year fell 18%, 21%. Second-tier cities, for example, in addition to Changchun, Taiyuan, Hohhot, Tianjin, Shijiazhuang, Guiyang, Nanning and a few other cities sales scale increased compared with the same period last year, the rest of the second-tier cities sales scale mostly negative year-on-year, and nearly half of the second-tier cities year-on-year decline of 20% or more, especially in Ningbo, Hefei, Qingdao and other cities, year-on-year decline of 50% or more, the scale of contraction is more significant.

▲ Source:CRIC

▲ Source:CRIC

(1) Policy level: Under the tone of "significant changes in supply and demand", it is expected that local governments will continue to optimize real estate market policies, and the supporting measures of the "three major projects" are expected to accelerate the landing.

In 2023, China's real estate market will continue to adjust to the bottom. The central policy is stable before and loose after, with the Politburo meeting in July, "the industry supply and demand relationship has undergone a major change" as a turning point, since then, many ministries and commissions to clarify the direction of optimization of real estate policy, the local policies continue to land. According to the monitoring of the central index, in 2023, more than 200 provinces, cities and counties (counties) have issued real estate regulation and control policies more than 670 times, and most of the cities have completely liberalized restrictive policies.

Looking forward to 2024, the central level of real estate policy is expected to force from three aspects, one is the financial support "three major projects" construction, and as a means to promote the construction of a new model of real estate development; The second is the implementation of the supply side of financial support, so that the "three is not less than", the second is to implement supply-side financial support, so that measures such as "three is not less than", "three arrows of financing" and "white list of real estate enterprises" will really be effective; and the third is to lower the tax on housing transactions, so as to stabilize demand and then stabilize the market.

(2) Market trend: It is expected that there will still be downward pressure on the sales scale of the national real estate market in 2024, and it is difficult to change the downward trend of new construction area and development investment.

Combined with the predictions of various research institutions on the real estate market in 2024, I organize the following:

▲ Source: Publicly available statistics

As an important part of the economic recovery, the real estate industry is currently facing the biggest problem from the residents' income expectations, home buying confidence can be restored. Slow sales recovery to a certain extent restricts the pace of repair of new construction, as well as the land transaction scale shrinks significantly, the existing inventory is high, the pressure on corporate capital is still under pressure and other factors will continue to drag down the enterprise new construction, 2024 real estate enterprises new construction scale year-on-year or difficult to turn positive.

From the point of view of the annual turnover changes, under the influence of the continued sluggish performance of the property market end, the land market also continued to run at a low level in 2024. Next, the rebound of the land market heat will still depend on the performance of the property market end. Only when the property market turnover of each city stabilizes and picks up, the willingness of real estate enterprises to acquire land will rise, and the overall heat of the land market will likely warm up.

It is worth noting that, with the guaranteed housing landing and the acceleration of urban village transformation, real estate investment will still have a certain support, or will gradually return to a normal and reasonable level.